Norway

The FIRE number in Norway, and the local rules that bend it

The quick version of a FIRE number is almost insultingly simple: take what you spend in a year and multiply by 25. Spend 400,000 kroner a year, and you need about 10 million to stop working. I ran that sum on myself years ago, felt the jolt, and then slowly worked out it was wrong for where I live. Not the maths, the country. Three Norwegian rules quietly bend that number, and a calculator built for American retirement accounts has no idea they exist.

The 4 percent rule is the starting line, not the finish

The 4 percent rule comes from decades of US market history. Roughly: if you withdraw about 4 percent of your pot in the first year and adjust for inflation after that, the money has usually lasted 30 years or more. Turn it upside down and your number is 25 times what you spend in a year. It is a rule of thumb, not a promise, and it is where an estimate begins. For a Norwegian, three local rules decide where it ends.

The napkin number is where an estimate starts, not where it ends.

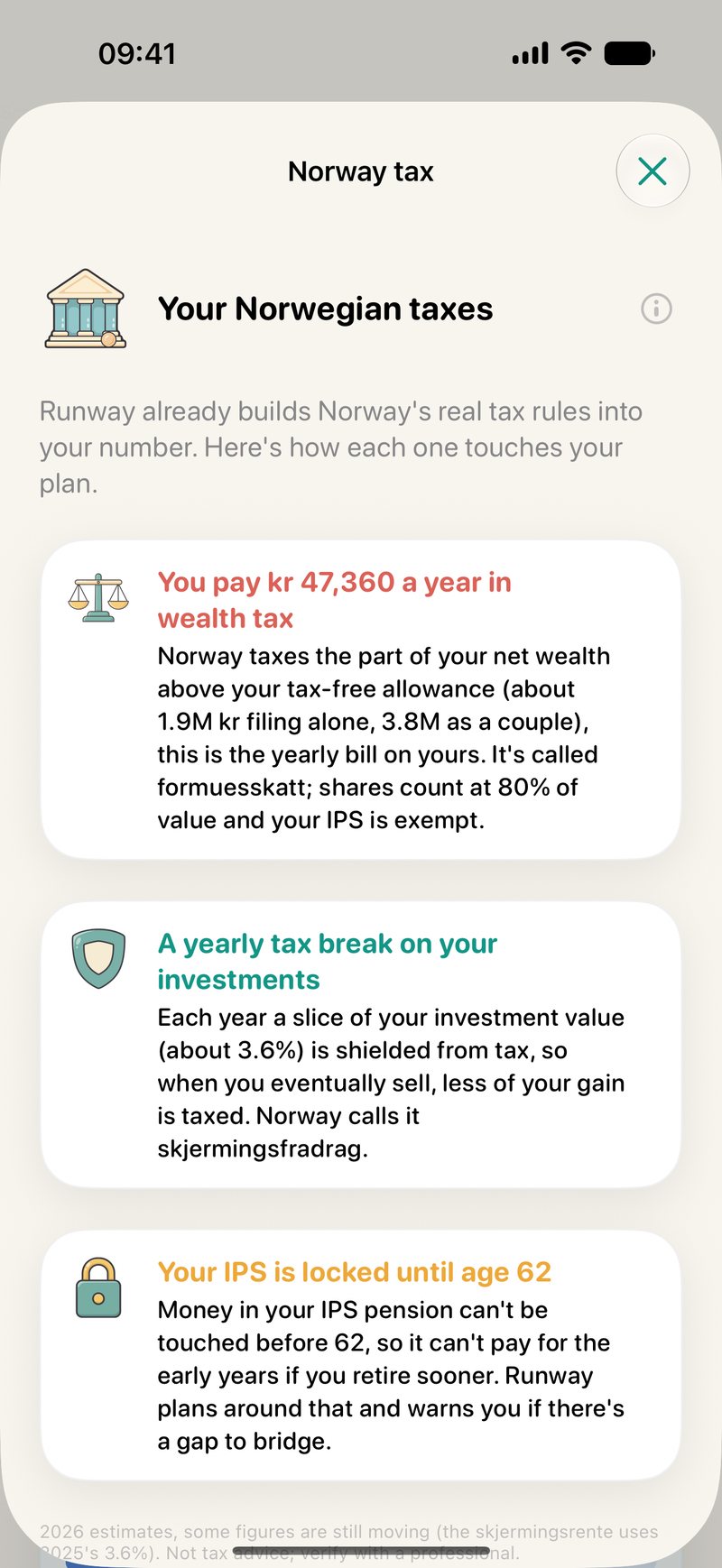

Rule 1: wealth tax nibbles a large pot every year

Norway taxes your net wealth above a threshold, every year, whether you sold anything or not. It is called formuesskatt, and a fat FIRE pot is exactly what it is looking at. In recent years the line has sat somewhere around 1.7 million kroner of net wealth per person, with the tax running to roughly one percent above that. Both numbers move most years, and shares and your own home are valued at a discount, so treat those as ballpark and check skatteetaten.no for the current figures.

The effect on your number is simple: your pot has to be big enough to pay its own yearly wealth-tax bill and still cover your spending. That nudges the target up. How far up depends entirely on how your money is split, which is the sort of thing worth modelling rather than guessing.

Rule 2: the ASK account quietly works in your favour

The aksjesparekonto, or ASK, is a share savings account with one feature that matters a lot in drawdown. Gains grow inside it untaxed until you take them out, and when you withdraw, your original deposits come out first, tax-free, before you touch a single taxed krone of gain. If you have paid in over many years, that is a large tax-free cushion sitting at the front of your retirement. Your early years of withdrawals can be low-tax, which lowers the real cost of living off the pot. This one bends your number down.

Rule 3: the state pension arrives later and shrinks the pot you need

Here is the rule people forget, and it is usually the biggest. Folketrygd, the state pension paid through NAV, plus any occupational or IPS pension, arrive from pension age, not before. So your savings do not have to fund your whole life. They only have to bridge you from the day you stop working to the day those pensions kick in. If a pension will cover a good slice of your spending from 67, your pot from 67 onwards only tops up the gap. That bridge is why a careful Norwegian number often lands earlier than a flat 25-times-spending figure suggests.

| The rule | What it does | Effect on your number |

|---|---|---|

| Wealth tax (formuesskatt) | Yearly tax on net wealth over a threshold | Pushes it up |

| ASK account | Gains deferred, your deposits withdrawn first | Pushes it down |

| State pension (folketrygd) | Pays from pension age, not before | Shrinks it, often a lot |

| Exit tax | A one-off if you emigrate | A cost on the way out |

The one that bites if you leave: exit tax

If your dream is to retire somewhere warmer, there is a fourth rule waiting at the door. Leaving Norway can trigger an exit tax (utflyttingsskatt) on the gains you have built up but not sold, as though you cashed out on the way out. It can be a real bill, and it is the sort of thing no cost-of-living comparison will warn you about. I went deeper on it in what the exit tax costs when you leave Norway, and on the wider move in which FIRE calculators handle a move abroad.

A rough worked example (a sketch, not your number)

Say you spend 400,000 kroner a year. The napkin number is 25 times that, 10 million. Now bend it. Once you are well over the wealth-tax threshold, formuesskatt might ask for something in the low tens of thousands a year, so the pot needs to be a touch bigger to carry that. Pushing the other way, if folketrygd will pay you, say, a couple of hundred thousand a year from 67, then from 67 you only need your pot to cover the gap, not the whole 400,000. The ASK ordering keeps the tax on your bridge-year withdrawals low while you get there. Net of all three, the pension bridge usually wins, and your real freedom age comes earlier than the flat 10 million implies. The exact figures are personal, which is the honest reason to model it rather than trust a napkin.

Runway does this maths for you

Runway is built on exactly these Norwegian rules: wealth tax, the ASK account, folketrygd and IPS, and the exit tax if you leave. It gives you one number, your freedom age, for free. It launches on the App Store on 25 August 2026, and the beta is open now.

Runway is built on exactly these Norwegian rules: wealth tax, the ASK account, folketrygd and IPS, and the exit tax if you leave. It gives you one number, your freedom age, for free.

Try the beta on TestFlight Download free on the App StoreFrequently asked

What is a good FIRE number in Norway?

Start with the 4 percent rule: multiply your yearly spending by 25. Spend 400,000 kroner a year and the napkin figure is about 10 million. Then adjust for three things a generic calculator ignores: yearly wealth tax on a large pot, the friendly withdrawal order of the ASK account, and the state pension that arrives later and shrinks the pot you actually need.

Does Norway have a wealth tax on savings and investments?

Yes, it is called formuesskatt. Norway taxes net wealth above a threshold every year. In recent years the line has sat around 1.7 million kroner per person with the tax running to roughly one percent above it, though both change most years and shares and your home are valued at a discount. Check skatteetaten.no for current figures.

What is the ASK (aksjesparekonto) and how does it help?

It is a share savings account where gains grow untaxed until withdrawal, and withdrawals take your original deposits out first, tax-free, before any taxed gain. In early retirement that ordering keeps the tax on your first years of withdrawals low.

Can I retire early in Norway using the state pension?

The state pension (folketrygd, through NAV) and any IPS or occupational pension arrive from pension age, not before. So your savings only need to bridge you from the day you stop working to the day those pensions start. That bridge often pulls your realistic freedom age earlier than a flat 25-times-spending number.

Does Norway tax me if I retire abroad?

It can. Leaving can trigger an exit tax (utflyttingsskatt) on the unrealised gains in your investments, as if you sold up on the way out. If retiring abroad is the plan, price it in. Treat all of this as estimates from public sources, not tax advice.

Written by Dylan, maker of Runway

Italian, in Norway about eight years, building the cross-border FIRE planner that did not exist for someone like me. Runway runs entirely on your iPhone. It is an educational planning tool, not financial or tax advice.

Sources worth checking yourself: the tax office skatteetaten.no for wealth tax and the ASK, and nav.no for the state pension. Figures change yearly, and some 2026 numbers are still moving.